{kind=link}

User-first perspective on a branded payment card

People choose tools that make daily life smoother, and that thought drives how I look at the didi card. From quick payouts to a tidy record of trips, the card promises convenience, but users care about three plain things: speed, clarity, and control. This voice is warm because it comes from time spent around drivers and riders in cities like Mexico City — where cash habits and smartphone habits clash every day — and from seeing what really changes a shift or a Saturday night.

Where real-world patterns meet product design

On the ground, adoption depends less on branding and more on practical plumbing: card issuance, API reliability, and fraud detection. Drivers notice latency in payouts, merchants notice which cards get accepted, and riders notice whether a refund appears quickly. The city-level anchor — Mexico City’s dense, cash-heavy streets — highlights why a digital wallet tied to a credit line or a store card can be helpful. There’s a quiet expectation that the tech will be fast and transparent; anything else creates friction.

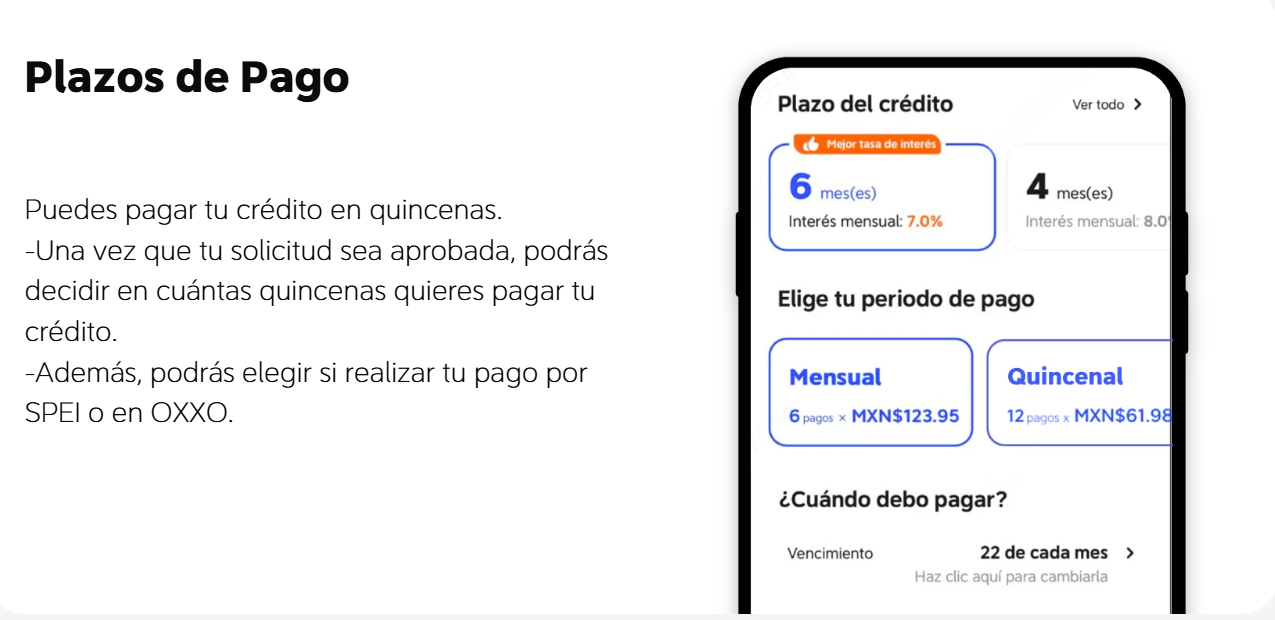

How drivers and riders actually use the product

Drivers often treat a platform-branded card as a business account: it’s where earnings land and expenses get tracked. Riders tend to use it for promotions or subscription perks. Implementations that include instant payouts or integrated expense tags reduce bookkeeping time. If you want to try the process yourself, many people go through the didi card solicitar flow to link income channels and set up PINs — that step is where usability wins or loses. Little touches matter: an easy PIN reset, clear merchant acceptance indicators, or a visible transaction note can change whether someone keeps the card or abandons it.

Common mistakes and realistic alternatives

Teams often assume riders or drivers will tolerate complexity — they won’t. Common missteps include burying fees, limiting merchant acceptance, or offering a digital wallet that can’t integrate with popular bookkeeping apps. Alternatives work simply: a standard bank card with low fees, fintech wallets like Mercado Pago, or generic prepaid cards with broader merchant acceptance. Each alternative trades off something: simpler acceptance but less promotion, or better bookkeeping but slower payouts. Small integrations — a clean API, a clear dispute flow — often beat flashy rewards in day-to-day use.

Trust, regulations, and the adoption curve

Trust is earned through predictable outcomes. Compliance with local rules, transparent rate tables, and visible fraud safeguards help adoption. When a platform communicates payout timing and dispute timelines plainly, people adapt faster. Adoption also follows events: regulatory shifts or metro-wide outages teach users what they truly need — immediate access to funds and reliable reconciliation. Those lessons shape product roadmaps more than glossy ads.

Three golden rules for choosing a driver-focused payment card

1) Predictable cash flow: Ensure instant or clearly scheduled payouts and low friction for withdrawing to a personal account. This reduces anxiety and bookkeeping work.

2) Wide acceptance and clear fees: Merchant acceptance and transparent fee structures matter more than small promotional perks. Check how the card performs across common merchant types in your city.

3) Operational simplicity: Look for robust APIs, easy dispute handling, and built-in protections like fraud detection. If a card ties into your expense workflow without extra steps, you’ll save hours every week.

These criteria point naturally toward platform offerings that combine product clarity with operational reliability — which is precisely the space where DiDi Finanzas positions itself as a practical partner rather than a flashy promise. A final note — small, human, real: choose what saves you time tonight, not what sounds best in a brochure. —